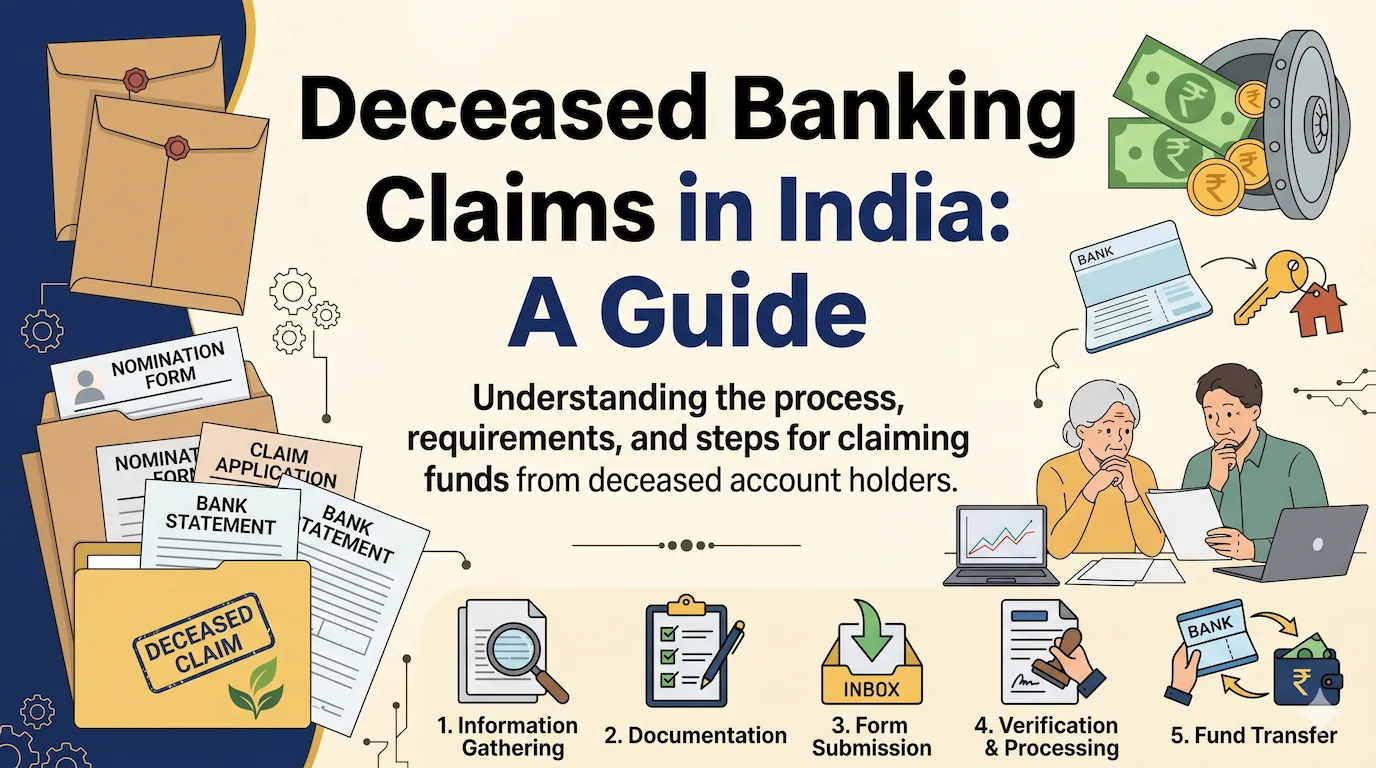

The process of handling deceased banking claims in India involves several legal and procedural steps. Upon the account holder’s death, beneficiaries must present the necessary documents, including the death certificate and succession certificate. Banks then assess the claims to ensure the proper distribution of funds, in accordance with relevant regulations and guidelines.

Key Takeaways

- Handling Deceased Banking Claims in India requires presenting documents like death and succession certificates, causing delays.

- Fragmentation between bank branches hinders the claims process, forcing heirs to manage multiple visits and paperwork.

- A ‘Single-Window’ solution could streamline the claims process, consolidating documentation and reducing physical burden for heirs.

- RBI guidelines exist to expedite claims, but many banks still impose unnecessary internal rules, stalling progress.

- Escalating issues to the RBI through grievance portals often leads to faster resolutions for Deceased Banking Claims in India.

The Grief After the Loss: Navigating the Red Tape of Deceased Banking Claims in India

Losing a loved one is a profound emotional blow. However, for many families, the period of mourning is quickly interrupted by a daunting secondary challenge: the bureaucratic maze of the financial system. When a family member passes away, their hard-earned savings and fixed deposits (FDs) become part of a complex recovery process. Effectively managing Deceased Banking Claims in India often turns into a marathon of paperwork, inter-branch delays, and regulatory hurdles.

The recent case of Late Smt. Vidya Devi and the Uttar Pradesh Gramin Bank (UPGB) serves as a powerful case study for why the current system needs a “single-window” revolution.

1. Fragmented Assets: The Biggest Hurdle in Deceased Banking Claims

In the case of Smt. Vidya Devi, the deceased held a Savings Account at the Mandi Samiti Branch and a Fixed Deposit at the Raipuri Branch. While both branches belong to the same bank, they often operate as administrative islands.

When legal heirs attempt to settle Deceased Banking Claims in India, they are frequently forced to visit each branch separately. This fragmentation is the root cause of delay. Instead of a holistic view of the customer’s relationship with the bank, the system forces heirs to repeat verification processes, submit multiple death certificates, and undergo redundant local inquiries. This is a significant point of friction for consumers.

2. The “Single-Window” Solution for Deceased Claims

The demand for a “Single-Window” settlement is not a luxury—it is a necessity for a fair banking experience. By requesting the transfer of the Raipuri FD to the Mandi Samiti branch, the legal heirs are seeking to consolidate the Deceased Claim Process (DCP).

Why consolidation is vital for Deceased Banking Claims in India:

- Documentation Consistency: One set of affidavits and indemnity bonds covers all assets.

- Reduced Physical Burden: Heirs do not have to travel between distant branches to submit original documents.

- Faster Liquidity: A single manager oversees the final payout, reducing the administrative “blame-game.”

In this specific case, the Mandi Samiti branch proactively issued Letter No. 50 to request this consolidation. When a bank recognizes that a unified claim is in the consumer’s interest, it upholds the spirit of the RBI’s Charter of Customer Rights.

3. RBI Guidelines vs. Ground Reality for Legal Heirs

The Reserve Bank of India (RBI) has issued clear directives to simplify Deceased Banking Claims in India. These guidelines explicitly state that:

- Time-Bound Settlement: Banks should settle claims within 15 days of receiving all documents.

- Simplified Documentation: For claims within specific thresholds, banks should not insist on succession certificates if a valid nominee or legal heir affidavit exists.

- Hassle-Free Access: Banks are encouraged to adopt procedures that minimize hardship for survivors.

Despite these rules, ground reality in Regional Rural Banks (RRBs) often involves “internal rules” that stall the process. A branch refusing to transfer an account for a deceased claim is essentially blocking the family’s access to their rightful inheritance.

4. Escalating Deceased Banking Claims: From Branch Manager to RBI

When internal bank requests—like Letter No. 50—go ignored, the only path left for the consumer is formal grievance redressal. The registration of grievance number DEABD/E/2026/0056861 with the Department of Financial Services (DFS) marks a critical turning point.

Escalation is often the only way to break the administrative inertia. Once a grievance regarding Deceased Banking Claims in India reaches the RBI level (CEPD), the bank’s Head Office is forced to explain why a simple inter-branch transfer was delayed, often leading to a resolution within days.

5. The Importance of the Article 4 Affidavit (e-Stamp)

A recurring issue in settling these claims is “legal heir” verification. In Smt. Vidya Devi’s case, an Article 4 Affidavit (e-Stamp) was prepared by Mahesh Pratap Singh. This document is the cornerstone of the claim.

Banks often use “verification” as a reason for delay. However, with the integration of digital systems and e-Stamps, verifying the authenticity of a legal heir has never been easier. The delay, therefore, is rarely about security and more often about a lack of standardized workflow between branches.

6. Conclusion: A Call for Empathetic Banking

The banking relationship should not end with a customer’s death; it should transition with dignity to their survivors. The struggle to move a Fixed Deposit from one branch to another highlights a systemic gap in how Deceased Banking Claims in India are managed.

Key Takeaways for Legal Heirs:

- Demand Consolidation: Always ask the bank to process all accounts (Savings, FD, Locker) at one branch.

- Reference Branch Letters: If one branch manager agrees to help, use their formal letter (like Letter No. 50) to pressure other branches.

- Leverage Portals: Don’t wait months. If a branch is unresponsive for more than 30 days, use the CPGRAMS portal to escalate to the RBI.

The goal is simple: One bank, one process, one place. As this case moves toward a resolution through the RBI, it serves as a reminder that persistence and regulatory escalation are vital tools for families fighting bank red tape.

To assist with your active grievance and ongoing bank transfer, here are the official contact details and application links for the relevant authorities.

1. Primary Authority: Reserve Bank of India (RBI) (Deceased Banking Claims in India)

Since your grievance is already assigned to the Nodal Officer at the CEPD (Mumbai), these are your primary points of contact for escalation:

- Office: Consumer Education and Protection Dept (CEPD).

- Official Name: Dr. Neena Rohit Jain (Chief General Manager).

- Address: 1st Floor, Amar Building, Sir P.M. Road, Fort, Mumbai – 400 001.

- Phone Number: 022-22630483 / 022-22604106.

- Email Address: pgrs.cepd@rbi.org.in or cgmcepd@rbi.org.in.

- RBI Helpdesk (Toll-Free): 14448 (9:30 AM to 5:15 PM).

2. Ministry of Finance: Dept. of Financial Services (DFS) (Deceased Banking Claims in India)

The DFS oversees the Banking Division where your complaint was received.

- Web Link: financialservices.gov.in

- Address: 3rd Floor, Jeevan Deep Building, Sansad Marg, New Delhi – 110001.

- Phone Number: 011-23742207 / 011-23340222.

- Secretary Email: secy-fs@nic.in.

3. Uttar Pradesh Gramin Bank (UPGB) (Deceased Banking Claims in India)

You should contact the Regional Office (Mirzapur) and Head Office (Lucknow) to inform them that an RBI grievance is active.

Regional Office Mirzapur:

- Address: Bharuhana, Near Tata Motor Shop, Varanasi Road, Mirzapur – 231001.

- Email: ROMIRZ@upgb.bank.in.

Head Office Lucknow: (Deceased Banking Claims in India)

- Address: 2nd & 3rd Floor, NBCC Commercial Complex, Vardan Khand, Gomti Nagar Extension, Lucknow – 226010.

- Phone (Toll-Free): 1800-180-0225 / 1800-102-0304.

- Email: HO@upgb.bank.in.

4. Tracking & Helpdesk Details (Deceased Banking Claims in India)

- Grievance Registration Number:

DEABD/E/2026/0056861 - Web Link to Track Status: CPGRAMS Portal (pgportal.gov.in)

- CPGRAMS Helpdesk: 1800-11-1960.

Note: When emailing the RBI or DFS, always include your Grievance Registration Number in the subject line to ensure it is matched to your existing file.

Facing a similar challenge? Share the details in the box below, and our team of experts will do their best to help.