Key Takeaways

- Mr Narendra Modi’s governance faces scrutiny due to PAN misuse and victim harassment.

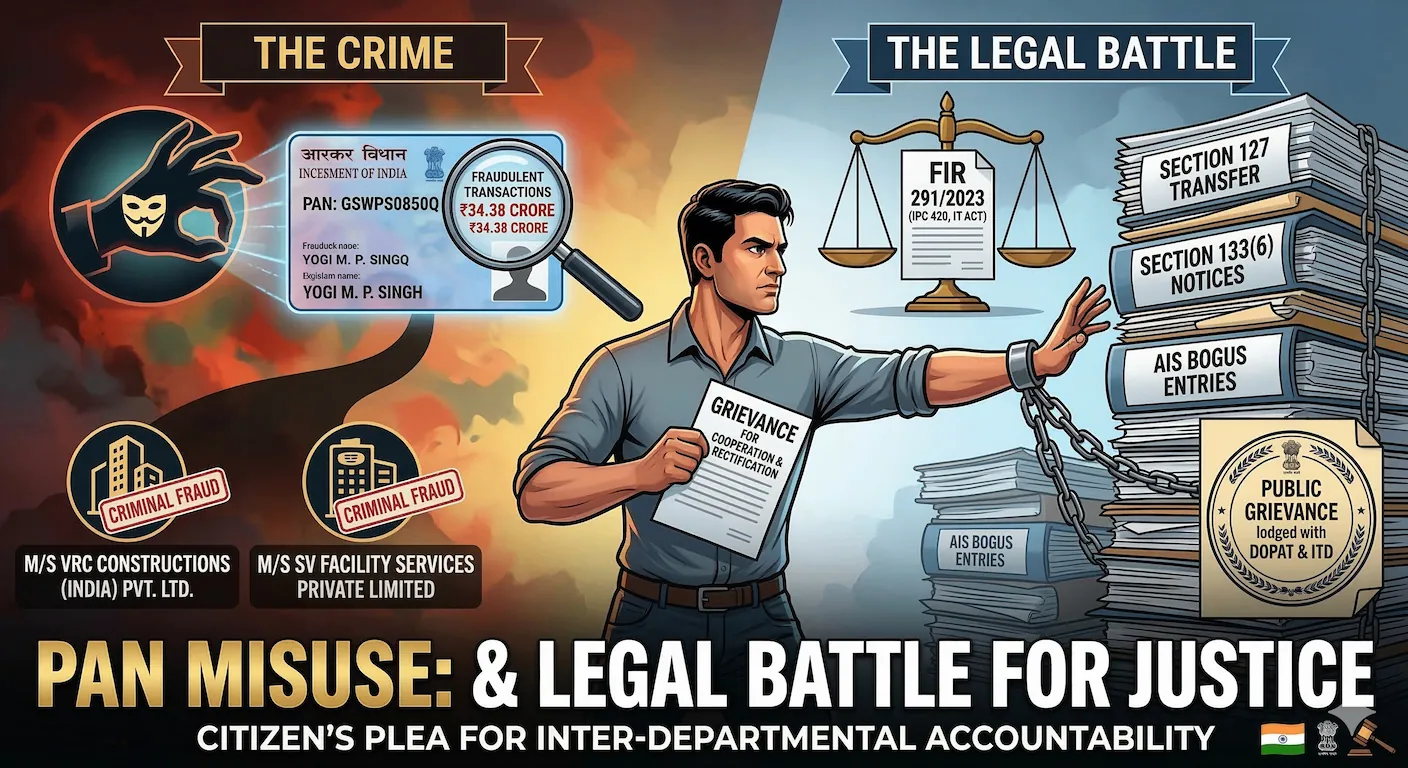

- The case of Yogi M. P. Singh highlights how PAN misuse leads to identity theft and wrongful tax allegations.

- Singh is a victim, yet the Income Tax Department treats him as a perpetrator. This situation exacerbates his legal challenges.

- The proposed centralisation of Singh’s case complicates investigations and ignores the core issue of identity theft.

- Immediate actions requested include halting centralisation, ensuring cooperation with law enforcement, and rectifying fraudulent entries in Singh’s Annual Information Statement.

PAN Misuse and the resulting legal battle are at the heart of the issue. How can our great Prime Minister, Mr Narendra Damodardas Modi, claim to provide good governance? How does he serve the people of this country? His ability to ensure good governance is questioned. Indirectly, the government is itself promoting the mental torture and the physical harassment of the victims of the PAN misuse. It seems we live in an era of corruption. The Premier investigating agencies failed to perform their own duties. This situation arises from the growing corruption in the Department of Income Tax’s operations. The facts make this obvious.

🛡️ The Double Victimisation: How PAN Misuse Traps a Citizen in a Legal Quagmire

The battle for justice in cases of sophisticated financial fraud often turns into a complex, protracted fight. The struggle is not just against the criminals. Ironically, the very state machinery intended to protect the victim often acts against them.

The Department of Personnel and Training (DOPAT) received a recent public grievance. At the same time, the Income Tax Department (ITD) also received a formal objection. These actions shed stark light on this precarious situation. The case of Yogi M. P. Singh(PAN: GSWPS0850Q) from Mirzapur illustrates a disturbing situation. A victim of massive PAN misuse and identity theft is undergoing continuous harassment. The tax authorities treat this victim as an offender, while the actual perpetrators roam free.

The Core Allegation: ₹35 Crore Tax Fraud on a Victim’s Identity

The gravity of the situation lies in the sheer scale of the alleged fraud: criminals have conducted over ₹34.38 Crore (approximately ₹350 Million) in illicit financial transactions using the victim’s Permanent Account Number (PAN). (PAN Misuse: & Legal Battle)

The applicant asserts that he is a victim of sophisticated criminal fraud and identity theft. This situation has already led to the registration of an FIR (No. 291/2023). The applicant submitted the FIR under Section 420 IPC. It also includes relevant sections of the IT Act. The officers at Police Station Kotwali Katra in Mirzapur carried this out. The case documents show that the fraudulent transactions involved entities such as M/S VRC Constructions (India) Pvt. Ltd.. M/s SV Facility Services Private Limited and others associated with addresses in New Delhi. These are places where the victim has never resided or operated.

The police view the applicant as a victim of identity theft. However, the Income Tax Department appears to be treating him as a co-conspirator in a massive tax evasion scheme.

🛑 PAN Misuse: & Legal Battle: A Legal and Logistical Nightmare

The immediate point of contention is the Notice under Section 127 of the Income Tax Act, 1961. The Principal Commissioner of Income Tax (PCIT) in Allahabad issued this notice. It proposes to move the applicant’s case from his local Assessing Officer in Mirzapur. The department will centralise the case to the DCIT/ACIT, Central Circle-5, New Delhi.

Understanding Section 127 of the IT Act

Section 127 grants the tax authorities the power to transfer a case from one Assessing Officer (AO) to another. This authority typically enhances administrative efficiency. It aims for better coordination or for “co-ordinated and effective investigation.” This is especially true when a group involved in financial dealings is under central investigation. This often occurs following a search or survey action..

Key Procedural Safeguards under Section 127: (PAN Misuse: & Legal Battle)

- The authorities must allow the assessee to present their case, unless the transfer occurs within the same city or locality.

- The transferring authority must record the reasons for the transfer in writing.

The Victim’s Objection: A Case Against Centralization

The applicant’s formal objection to the PCIT, Allahabad, is legally sound and morally compelling:

- Wrongful Assumption of Assessee in Default: The case was centralised in Delhi. This occurred under the pretext of coordinating investigation with the VRC Group. It effectively treats the applicant as an associate in tax evasion. The applicant argues that any link found is a direct result of the criminal misuse of his PAN and identity.

- Impeding Criminal Investigation: The transfer shifts the focus from the core crime—identity theft—to tax prosecution of the victim. Centralisation in Delhi is far from his local jurisdiction. This move would exacerbate the hardship. It would complicate his ability to cooperate with the local police.

- Localised Criminal Jurisdiction: The criminal investigation is already active and ongoing with the Mirzapur Police. The applicant argues that his case relates to a localised criminal fraud and identity theft. It does not involve complex, multi-city tax planning. Such planning necessitates centralisation.

The core argument is that the principle of “coordinated and effective investigation” fails. This happens when the identity of one of the investigated parties is fundamentally fraudulent. The focus should be on exposing the crime, not punishing the victim for the crime committed against them.

🚨 The Critical Roadblock: Non-Cooperation with Law Enforcement

The most critical point of the entire grievance is the alleged lack of cooperation by the Income Tax Department (ITD). This issue involves the local police. This situation is quite alarming.(PAN Misuse: & Legal Battle)

The grievance highlights that the Investigating Officer (I.O.) of FIR No. 291/2023 has formally asked the ITD to provide the bank account details and documents. Fraudsters committed these transactions using the victim’s PAN. The applicant attaches a copy of the I.O.’s letter dated 04/07/2025 as evidence.

- The Problem: The ITD holds the most crucial evidence. These are the source and destination bank account details. They are essential to identify and prosecute the actual perpetrators of the tax fraud and identity theft.

- The Consequence: The ITD allegedly withholds this information, severely hampering the police’s criminal investigation. The applicant finds themselves caught in a loop. The tax department continues to issue notices against him. Yet, they refuse to provide the evidence. This evidence would prove his status as a victim and unmask the real criminals.

The prayer, therefore, is not merely to drop the centralization. Instead, it urges to “Direct Immediate Cooperation with Police,” making this an urgent matter of inter-departmental accountability.

The Perpetual Harassment: Notices and the Annual Information Statement (PAN Misuse: & Legal Battle)

The victimization worsens due to continuous procedural harassment. Authorities issue various notices, such as one U/s 133(6) for ₹1,12,16,962 claimed as ‘Rent received.’

Understanding Section 133(6) (PAN Misuse: & Legal Battle)

Section 133(6) is an investigative power. It allows tax authorities to call for specific information and documents from any person. This can be the assessee or a third party, like a bank. You need the information if it is “useful or relevant” to any inquiry or proceeding under the Act. While it is a powerful tool for gathering data, its repeated use against a proven victim is harmful. Using fraudulent data turns a compliance tool into an instrument of harassment.

The AIS Rectification Request

The applicant also seeks to rectify his Annual Information Statement (AIS). He wants to permanently remove all fraudulent entries. These entries are related to the ₹350 million worth of bogus transactions.

- What is AIS? The ITD introduced the AIS as a comprehensive statement. It provides a consolidated view of all financial transactions related to a taxpayer. This often includes data received from third parties, such as banks and financial institutions.

- The Challenge: When third parties report fraudulent transactions, they are misusing the PAN to alert the ITD. These transactions automatically populate the victim’s AIS. Until they remove these entries, they serve as a prima facie record of unaccounted income. This continually triggers further notices, scrutiny, and hardship for the victim.

The request to rectify the AIS is necessary. It will officially wipe the slate clean of the crime committed against him. This will end the endless cycle of tax notices triggered by false data.

🏛️ Call for Accountability and Justice

This case, now registered as a public grievance, transcends a typical tax dispute. It poses a fundamental challenge to the administrative and legal system. How does the government protect a citizen when one arm of the state (the Police) is investigating a fraud? Meanwhile, another arm (the ITD) is pursuing the victim based on the outcome of the fraud. (PAN Misuse: & Legal Battle)

The immediate actions requested are clear:

- Halt Centralisation: “Prevent the transfer of the case to New Delhi Central Circle-5.” Recognise the applicant’s status as a victim of localised identity theft.

- Ensure Inter-Departmental Cooperation: Mandate the ITD to provide the Mirzapur Police’s Investigating Officer with all bank account and transaction details. This message specifically addresses DDIT/ADIT(Inv.), 5(1), New Delhi, and Central Circle-5. This information is essential to ensure the quick arrest of the actual perpetrators.

- Cure the Root Cause: Initiate steps to permanently remove the fraudulent financial entries from the applicant’s Annual Information Statement (AIS). This action will stop the engine of perpetual tax harassment.

The victim’s request is a cry for justice and a plea for administrative common sense. The Director in the Administrative Vigilance department must realise this. In cases of PAN misuse, the taxpayer is not the enemy. Instead, they are a crucial partner in exposing a financial crime. Justice requires the system to focus its energy on prosecuting the ₹35 Crore fraudsters. It should not persecute the victim of the fraud.

Would you like me to find the contact details? Or should I locate the specific website link for lodging a formal complaint? This is regarding non-cooperation by an Income Tax official with a police investigation?

Facing a similar challenge? Share the details in the box below, and our team of experts will do their best to help.