Key Takeaways (Understanding SBI Account Restrictions)

- Arbitrary account restrictions from banks can disrupt customer access to funds, often occurring without clear explanations.

- Mr. Singh’s grievance highlights denied AEPS withdrawals and traditional counter services, yet digital transactions remain functional.

- Potential reasons for such restrictions include technical errors, compliance issues, or pending KYC updates.

- Customers should escalate unresolved issues by visiting the branch, contacting the Banking Ombudsman, or using SBI’s digital complaint channels.

- Clear communication and timely resolution are customer rights; maintaining updated KYC information is crucial.

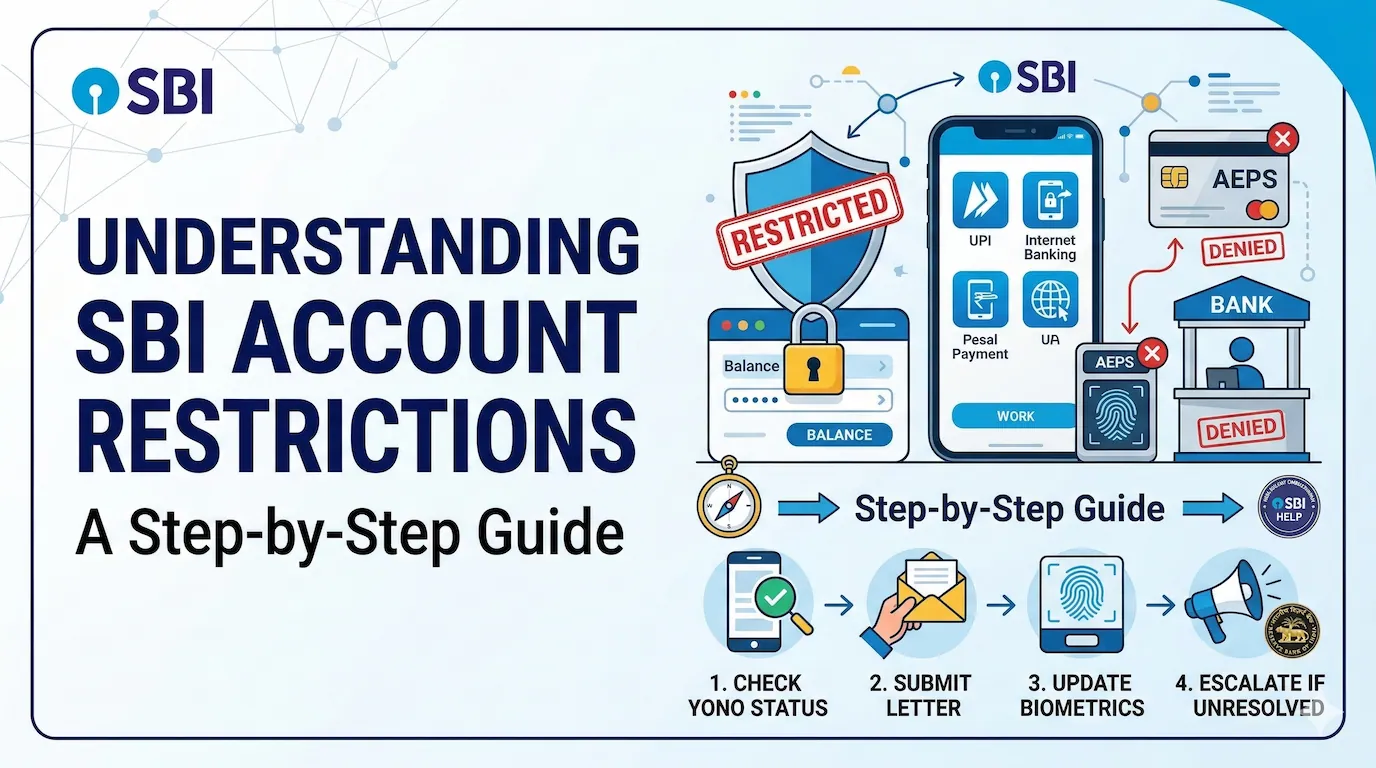

🏦 Understanding SBI Account Restrictions: Why Your Bank Might Be Denying Withdrawals and What to Do Next

The relationship between a customer and their bank is built on trust. This includes the fundamental trust that you can access your own money when you need it. However, as one recent grievance highlights, this trust is sometimes arbitrarily broken by unexplained restrictions on withdrawal services. Understanding SBI Account Restrictions can help explain why these issues arise. It also guides you on what you should do if it happens to you.

Mahesh Pratap Singh of Mirzapur City Branch (SBI) formally registered a complaint. He explained how his ability to withdraw funds was suddenly blocked. This affected both traditional counter methods and the Aadhaar Enabled Payment System (AEPS). Despite this issue, his account remains fully operational for digital transactions (UPI/Internet Banking). (Understanding SBI Account Restrictions)

This post breaks down the customer’s specific issues. It explores the possible technical and regulatory reasons behind such restrictions. It also provides a clear, actionable guide on how to force a resolution.

Grievance Snapshot: The Case of Unexplained Denial of Service (Understanding SBI Account Restrictions)

The core of Mr. Singh’s grievance (Registration No.: DEABD/E/2025/0106737) lies in the inconsistent and unauthorized denial of two specific withdrawal channels:

- AEPS Failure: An attempt to withdraw $₹4,000.00$ via AEPS on November 28, 2025, failed with the explicit message: “AEPS SERVICES NOT OPTED FOR BY CUSTOMER. KINDLY VISIT BRANCH FOR ENABLEMENT OF AEPS TRANSACTIONS.” This is the key point, as the customer insists the service was previously functional.

- Traditional Counter Denial: The bank staff also refused over-the-counter withdrawals via the bank passbook without providing a clear, justifiable reason.

Crucially, digital transactions (Internet Banking/UPI) are still functional. This inconsistency suggests a partial, channel-specific restriction rather than a full regulatory or legal freeze on the entire account.

Potential Reasons Behind the Arbitrary Restrictions

When a bank blocks specific services but leaves others open, it typically points to a technical issue. It could also indicate an operational problem or a Know Your Customer (KYC) compliance issue tied to a specific channel. (Understanding SBI Account Restrictions)

1. The AEPS “Opt-Out” Error (Technical/Operational) (Understanding SBI Account Restrictions)

The error message “AEPS SERVICES NOT OPTED FOR BY CUSTOMER” is the most direct clue. This suggests that the bank, or the core banking system (CBS), has either:

- Systemic Recalibration: The bank may have recently changed its policy. It requires all customers to explicitly “opt-in” or re-validate for AEPS services. This is necessary even if they were previously active. This can be a security measure to prevent unauthorized AEPS use.

- Data Migration Error: During a system update, the data was affected. The link between the customer’s Aadhaar and their account for AEPS purposes may have been corrupted. Alternatively, it may have been reset, defaulting the status to “Not Opted For.”

- Aadhaar-Seeding Issue: The UIDAI email confirms successful biometric authentication. However, the status of the Aadhaar linkage within the SBI CBS for AEPS purposes might need re-verification.

2. Denial of Traditional Withdrawal (Regulatory/KYC)

The denial of counter withdrawal often occurs when a passbook is presented. This situation points to a potential flag on the account’s operational status. (Understanding SBI Account Restrictions)

- KYC Refresh Pending: Even if the account is “fully KYC-compliant,” banks frequently flag accounts for periodic KYC updates. These updates are also known as c-KYC (Central KYC Registry) or O-KYC (Operational KYC).If a mandatory document is overdue, such as an updated address proof or income declaration, banks often place a “soft-freeze.” This restricts physical or branch-based transactions. However, digital channels remain open.

- Passbook Irregularity: Though less common, the counter service may be denied if the passbook is deemed mutilated or old. It may also be denied if the signature verification flags a discrepancy. However, staff must communicate this clearly.

- Dormancy Prevention: If the account has been relatively inactive, banks can impose withdrawal restrictions. This encourages the customer to update their details. It prevents the account from slipping into Dormant Status. (Understanding SBI Account Restrictions)

A Step-by-Step Action Plan for Resolution (Understanding SBI Account Restrictions)

Mr. Singh has taken the correct initial step. He submitted a formal written grievance directly to the Branch Manager. He then escalated it to the General Manager of the Customer Service Department at SBI Corporate Centre. Here is how to proceed if the initial three-day deadline passes without resolution.

1. The Critical Branch Visit (Addressing the Root Cause)

Since both failure messages directed the customer to “visit the branch,” the in-person meeting is unavoidable. The customer must visit the Mirzapur City Branch prepared with the following:

- Formal Grievance Copy: Present the letter dated December 1, 2025, and reference the registration number.

- Documentation: Carry original and copies of Aadhaar, PAN Card, and Passbook.

- Demand a Written Confirmation: Do not leave without a written note, memo, or email from the Branch Manager. Ensure the note explains the exact reason for the restriction. It should also detail the specific task required for service restoration.

2. Escalation to the Banking Ombudsman (If Unresolved)

If the branch fails to provide a satisfactory, written explanation, the matter should be escalated. Another requirement is restoring all services within the stipulated timeframe. This should be done through the Banking Ombudsman Scheme established by the Reserve Bank of India (RBI). (Understanding SBI Account Restrictions)

- Eligibility: The complaint can be filed if the bank rejects the complaint. It can also be filed if the bank does not reply within 30 days of the initial complaint. In this case, a formal grievance was filed on December 1, 2025. A complaint can be filed with the Ombudsman after 30 days if the issue persists.

- Filing: Complaints can be filed online via the RBI’s Complaint Management System (CMS) portal.

The denial of essential withdrawal services without prior notice constitutes a clear failure of service under RBI guidelines. The service must also have a valid, communicated reason for any denial. This is precisely the type of issue the Banking Ombudsman is mandated to resolve.

A Note on Customer Rights and Financial Hygiene (Understanding SBI Account Restrictions)

Arbitrary restrictions on fully KYC-compliant accounts are highly disruptive. Customers have the right to:

- Clear Communication: The right to know why a service is being denied and the exact steps for restoration.

- Timely Resolution: Expectations of a resolution within a reasonable timeframe, typically set by the bank’s own Customer Service Codes.

This specific grievance highlights the importance of financial hygiene. Always keep your KYC documents updated. Respond immediately to any official bank communications requesting re-verification or opt-in for services like AEPS.

Mr. Singh’s complaint is detailed and well-structured. It provides an excellent template for any customer facing a similar unexplained denial of access to their own funds. The next step is diligent follow-up and prompt escalation to the Ombudsman if the branch fails to act.

Here are the details for the internal State Bank of India (SBI) escalation points. There is also the final regulatory step with the Reserve Bank of India (RBI).

🏛️ Complaint Escalation Matrix: SBI and RBI (Understanding SBI Account Restrictions)

Your initial complaint has been filed. It has been escalated to the General Manager. This step is a key part of the SBI’s internal process. If the deadline given in your follow-up email passes without resolution, you must move to the next level.

1. Internal Escalation: SBI Local Head Office (LHO) – Lucknow Circle

Mirzapur City Branch falls under the Lucknow Local Head Office (LHO) of SBI. This level is next in the escalation process within the bank. It comes after the Branch Manager. It is also after the Corporate General Manager of Customer Service. (Understanding SBI Account Restrictions)

| Officer | Designation | Contact Details |

| Nodal Officer (Lucknow LHO) | Asst. General Manager (Customer Service) | Mr. Rahul Kumar Singh |

| Email Address | agmcustomer.lholuc@sbi.co.in | |

| Contact Number | 0522-2295395 / 0522-2295392 | |

| Address | Customer Service Dept., Local Head Office, Moti Mahal Marg, Lucknow – 226001 |

If your issue is not resolved by December 3, 2025, you should take action. Send a copy of your original grievance to the Lucknow LHO Nodal Officer. The officer’s name is Mr. Rahul Kumar Singh. Be sure to include the follow-up email. Cite the previous grievance registration number: DEABD/E/2025/0106737.

2. Digital Complaint Channels (SBI)

You can use the official SBI portal to register and track your complaint digitally, which creates an audit trail. (Understanding SBI Account Restrictions)

- SBI Customer Request and Complaint Form (CRH):

- Link: Use the latest unified portal:

https://crh.sbi.bank.in - Process: You can use this link to raise a fresh complaint or track the status of your existing one using your registration number. This ensures your complaint is logged into their central system.

- Link: Use the latest unified portal:

- Other Email: You can also send a complaint to the general Customer Care email: customercare@sbi.co.in

3. External Escalation: RBI Ombudsman Scheme (Understanding SBI Account Restrictions)

This is the final and most powerful step. Take it only if the bank fails to resolve your issue within the required time. This is typically 30 days from your initial complaint date. However, immediate denial of service often warrants quicker escalation.

The Reserve Bank of India (RBI) operates the Integrated Ombudsman Scheme (RB-IOS). It resolves customer complaints against regulated entities like SBI.

- Complaint Filing Platform:RBI Complaint Management System (CMS)

- Link:

https://cms.rbi.org.in - Eligibility Criteria for Filing: You can file a complaint with the RBI Ombudsman if:

- You have first approached the bank (Branch, Nodal Officer, General Manager).

- The bank has either rejected your complaint. They have also failed to provide a satisfactory reply. This should have been done within 30 days of filing the internal complaint (which was Dec 1, 2025).

- Link:

If you or Mr. Singh need to escalate this issue, there is a structured hierarchy you must follow. In India, you cannot go to the Ombudsman until you have given the bank a fair chance (usually 30 days) to fix it themselves.

Here are the official contact details for the relevant public authorities:

🏢 Level 1: State Bank of India (Internal)

Before going to the regulator, you must file a formal complaint with SBI and obtain a Ticket ID/Service Request Number. (Understanding SBI Account Restrictions)

- Online Complaint Portal (CMS):https://cms.sbi.co.in/

- Select “Raise Complaint” and choose the category “Account Related” or “Technical Issue.”

- Toll-Free Helplines: * 1800 1234 or 1800 2100

- 1800 11 2211 (Dedicated Customer Care)

- SMS Escalation: If you are unhappy with the service at the Mirzapur branch, SMS UNHAPPY to 8008 20 20 20. A representative from the Local Head Office (LHO) will typically call you back.

- Nodal Officer (Lucknow Circle): Mirzapur falls under the Lucknow Circle. You can email the Assistant General Manager (Customer Service). Contact them at agmcustomer.lholuc@sbi.co.in.

🏛️ Level 2: The Banking Ombudsman (External)(Understanding SBI Account Restrictions)

If SBI does not resolve the issue within 30 days, you should approach the Reserve Bank of India (RBI). If you are unsatisfied with their response, you should approach the Reserve Bank of India (RBI).

- The Integrated Ombudsman Scheme (RB-IOS): This is a “One Nation One Ombudsman” system. It was launched by the RBI. The scheme handles all bank grievances.

- Online Portal:https://cms.rbi.org.in/

- This is the most effective way to file a complaint. You will need to upload your original complaint copy to SBI and their response (if any).

- Toll-Free Number: 14448 (Multi-lingual support to help you file the complaint).

- Physical Address (CRPC): Centralised Receipt and Processing Centre,Reserve Bank of India, 4th Floor, Sector 17,Chandigarh – 160017.

⚠️ Important Tip for Mr. Singh (Understanding SBI Account Restrictions)

When filing the complaint, specifically mention that “Digital transactions (UPI) are successful but AEPS and Branch withdrawals are denied.” This proves that the account is active. However, the bank is restricting specific “Assisted” channels. This action violates the RBI Charter of Customer Rights.

Facing a similar challenge? Share the details in the box below, and our team of experts will do their best to help.