🚨 The PAN Identity Crisis: Unmasking the Misuse of a Unique Identifier

The Permanent Account Number (PAN) is foundational to India’s financial and taxation system. It is designed to be a unique and permanent identity for every individual and entity engaging in significant financial transactions. Yet, a recent and alarming grievance filed with the Central Board of Direct Taxes (CBDT) throws this fundamental assumption into serious doubt.

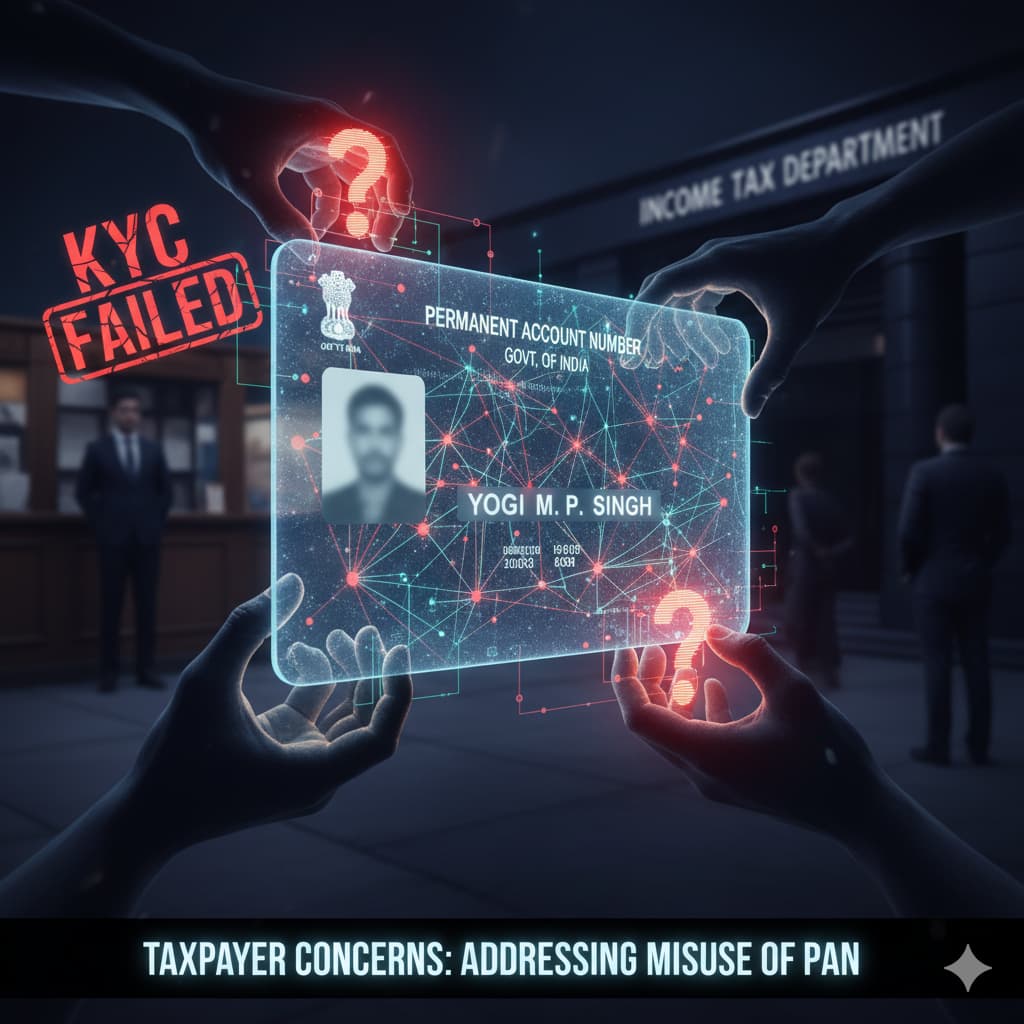

The complaint, lodged by Yogi M. P. Singh, exposes a chilling scenario: the blatant misuse of his PAN by fraudulent elements, leading to a host of financial activities—including business receipts, GST turnover, and even winnings from lotteries and online games—being erroneously linked to his identity.

This situation isn’t just about an individual’s financial headache; it points to a systemic failure that demands immediate attention from banking institutions, the Income Tax Department (ITD), and law enforcement.

The Critical Questions Arising from a Grievance

The complainant’s own words frame the central paradox: If the PAN is unique, how can it be misused by someone else?

The very premise of PAN’s integrity is shattered when an innocent citizen finds their identity tagged with substantial, undeclared income and transactions they never conducted. The detailed Taxpayer Information Summary (TIS) provided in the grievance—showing categories like ‘Winnings from lottery,’ ‘Business receipts,’ and ‘GST turnover’—is a stark, quantified representation of this identity theft.

| SR. NO. | INFORMATION CATEGORY | PROCESSED BY SYSTEM (INR) | CONCERN |

| 1 | Winnings from lottery or crossword puzzle | 613 | Misused PAN |

| 4 | Business receipts | 10,63,414 | Misused PAN |

| 5 | GST turnover | 25,44,342 | Misused PAN |

| 7 | Winnings from Online Games | 550 | Misused PAN |

The complainant explicitly states that the TIS “does not concern the applicant who is the real PAN holder” and that he has “never submitted any income tax return”. This proves that the financial activities linked to the PAN are entirely fraudulent concerning the actual individual.

The Serious Lapses in Due Diligence

The sheer scope of the reported fraudulent activities necessitates questioning the mechanisms that allowed them to take place. The core of the issue lies in two key institutional failings:

1. Banking Institutions and KYC Failure

The most direct point of violation is the opening of bank accounts. A bank account is the gateway to almost all financial activities, including those listed in the TIS. The complainant asks, “how are fraudulent elements able to open bank accounts without undergoing proper verification of records?”

- Know Your Customer (KYC) Standards: Banks are mandated to follow strict KYC procedures, which require verification of documents like PAN and proof of address against the original copies and the individual’s physical presence.

- Aadhaar/PAN Linkage Loopholes: While Aadhaar is often used for bank account opening, PAN is essential for high-value transactions. Misuse suggests either forgery of the PAN card coupled with weak identity checks by the bank staff, or a complete bypass of the verification process through corrupt means.

- Lack of Digital Audit Trail: If a bank staff member is enabling the fraud, there is a clear “serious lapse in the due diligence process” that should be easily detectable via internal audits.

2. The Income Tax Department’s Monitoring Role

The ITD is the custodian of the PAN database. The department’s role is not just to issue the number, but to safeguard its integrity and monitor its use.

- Failure of Real-time Monitoring: The ITD’s systems are clearly flagging these transactions and sending “streaming messages” to the real PAN holder. However, the system’s ability to act on the initial red flags—such as multiple bank accounts being opened in different cities under the same PAN, or the sheer volume and diverse nature of transactions like lotteries and GST turnover—appears to be nonexistent.

- Inadequate Investigation: The applicant has submitted “more than hundreds of representations” and communicated the issue to the Intelligence and Criminal Investigation wing. Yet, the official status shows “Three representations considered as TEP result 0.” This reflects a bureaucratic inertia that is failing to translate documented evidence of a crime into decisive action.

The Accountability Void: Why are the Enforcers Blind?

The most troubling aspect of this case is the alleged “consistent failure” of the police and the inaction against “negligent staff in both banking institutions and the Income Tax Department.”

The grievance directly addresses the failure of the enforcement ecosystem:

The police have consistently failed to take action against negligent staff… Consequently, this inaction not only emboldens wrongdoers but also undermines public trust in the system.“

The failure to investigate and prosecute bank or ITD staff who enable such fraud creates an accountability void. When the system designed to protect citizens becomes the source of their suffering, it is a profound failure of governance.

The grievance status remains “Under process” (as of 13/03/2025), directed to the Director General of Income Tax (Systems). This suggests the case is being treated as a technical data issue rather than a criminal identity theft and corruption matter.

The Final, Imperative Question

The suffering caused to innocent citizens, like Yogi M. P. Singh, due to this administrative negligence cannot be ignored. The misuse of a unique financial identity has severe consequences, potentially leading to unwarranted tax demands, financial liabilities, and harassment.

The final question posed by the complainant encapsulates the public’s anxiety: “who will be held accountable for the suffering caused to innocent citizens due to this administrative negligence?”

The resolution of this specific grievance must serve as a blueprint for a nationwide strategy to secure the integrity of the PAN system, enforce stringent KYC norms, and hold negligent officials—in banks and government departments alike—personally accountable. The trust in India’s financial system hinges on it.

What Needs to Happen Next

- System-Wide Forensic Audit: The DGIT (Systems) must initiate a forensic audit to trace all bank accounts and entities linked to the misused PAN and immediately flag them as fraudulent.

- Criminal Investigation Mandate: The case must be escalated from a mere grievance to a formal criminal investigation involving the police and the ITD’s Intelligence wing to identify the fraudulent elements and the enabling institutional staff.

- Strengthening KYC Integration: Banks must implement a real-time, mandatory digital verification layer with the ITD database for all PAN submissions, going beyond simple document checks.

Would you like me to find the official guidelines issued by the CBDT regarding reporting and resolving PAN misuse cases?

Facing a similar challenge? Share the details in the box below, and our team of experts will do their best to help.